Asia Pacific automotive air intake manifold market to garner massive valuation over 2017-2024, driven by a stringent regulatory framework

Publisher : Fractovia | Published Date : October 2017Request Sample

Röchling Automotive, a German based plastic processing group has recently set a new benchmark for players in automotive air intake manifold market by introducing polypropylene (PP) based intake manifolds. The company has exploited PP’s low-density characteristic to successfully optimize the weight, cost, and acoustics of air intake manifolds. In consequence, most of the automotive manufacturers are now expected to give preference for polypropylene based intake manifolds, which will significantly stimulate automotive air intake manifold industry share over the years ahead. Moreover, the components manufactured with PP as a base material are less energy-intensive and contribute to minimize carbon emissions in the environment. This benefit is in line with the growing deployment of strict rules and regulations related to CO2 emissions, and would considerably impel worldwide automotive air intake manifold market.

U.S. Automotive Air Intake Manifold Market Size, By Vehicle, 2013 – 2024 (USD Million)

Many renowned giants in automotive air intake manifold industry are making heavy investments to develop advanced green technology to comply with the environmental requirement of automobile manufacturers. The popular Italian car manufacturer, Ferrari has launched a new car model Portofino, manufactured with an innovative design and cutting-edge production techniques featuring light weight components. In order to achieve maximum mechanical efficiency and enhance performance of an engine the company has designed high tumble intake manifolds, which helps to reduce the energy losses during air intake. Considering the benefits of engine efficiency, most of the consumers are thus, replacing their damaged intake manifolds with advanced products such as the aforementioned, which has considerably propelled automotive air intake manifold industry from automotive aftermarket. According to estimates, automotive air intake manifold market size is slated to record a CAGR of 6.4% over 2017-2024 from aftermarket channel alone.

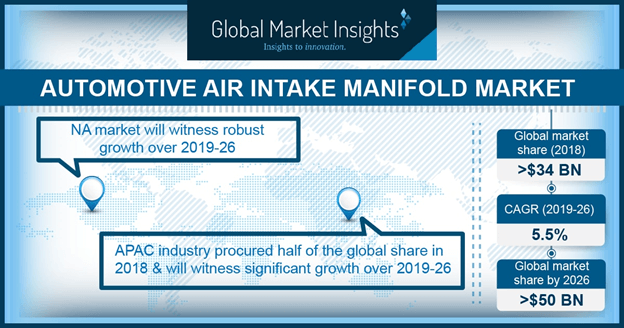

The exponential rise in the demand for automobiles across North America has positively impacted the regional automotive air intake manifold industry outlook. Statistically, vehicle sales across U.S. accounted for more than 17.55 million units in 2016, which was considerably more than the vehicle sales in 2015. Taking into account the surging demand for vehicles, automakers are increasingly expanding their manufacturing plants, which will favorably influence automotive air intake manifold market size. For instance, MAHLE has opened two new manufacturing plants in Mexico to provide assembly operations for automotive customers across the northeastern and central regions of Mexico.

Regional governments are on a spree, enforcing emission control norms to control air pollution caused due to vehicle emissions, which will propel automotive air intake manifold industry share. In 2017, the Indian Ministry of Road Transport and Highways (MoRTH) deployed Bharat Stage (BS) IV emission standards for all types of on-road vehicle categories across India. Apart from this, the Indian Government has drafted regulations to implement BS VI emission standards, which will be effective from 2020. The ministry has also suggested that all the vehicle categories such as heavy duty, light duty, three and two wheeled vehicles should be manufactured in accordance with the BS VI norms. To comply with the emission control norms, most of the automotive manufacturers, specifically the two-wheeler developers, are expected to shift toward fuel pump modules and electronic fuel injection (EFI) systems to enhance the functioning of an engine. The surging deployment of EFI systems in two wheelers across Indian two-wheeler industry over the coming years is thus likely to influence Asia Pacific automotive air intake manifold market trends.

In order to enhance the air quality by minimizing pollutants emitted from road transport vehicles, the EU has deployed fairly strict emission regulations across the continent. The BS VI standards are likely to bring Indian motor vehicle regulations at par with the European Union (EU) regulations for heavy-duty trucks, buses, two-wheeled vehicles, commercial vehicles, and light-duty passenger cars. Global Market Insights, Inc., estimates that, in the coming years, pertaining to the rapid industrialization, the demand for heavy commercial vehicles will increase noticeably, which would lead automotive air intake manifold market share from HCVs to grow at a CAGR of more than 5.7% over 2017-2024.

Taking into account the future demand for EFI systems and pump modules, many local automotive component manufacturers in India are partnering with electric machinery manufacturing firms. For instance, Indian city-based manufacturer, Paricol has signed a technical collaboration with Wenzhou Huirun Electrical Machinery Company to produce and supply fuel pumps and its modules across India. This incidence sets a precedent for automakers to upgrade the features of mobility and transportation to comply with strict fuel economy regulations, which would influence automotive air intake manifold industry size. Speaking of which, the competitive spectrum of automotive air intake manifold market is inclusive of renowned players such as MAHLE GmbH, Keihin Corporation, Röchling Group, Tenneco Inc., and Magneti Marelli. These companies have undeniably been striving to bring about substantial changes in product design and development, which is certain to stimulate automotive air intake manifold industry size in the forthcoming years.